Module 5: Basics of Fundamental Analysis in Gold Trading

5.1 Introduction to fundamental analysis [1]

Fundamental analysis refers to the practice of analysing the driving factors behind a market, so as to discern and understand the price action of an asset. It is used to determine the intrinsic value of a security or asset based on underlying economic factors, and can be a valuable tool in formulating trade ideas.

The factors to focus on in fundamental analysis depends on the asset or market you are analysing. In the case of gold trading, fundamental analysis encompasses an array of macroeconomic and geopolitical factors, ranging from monetary policy, inflation rate, and political developments, to production supply and – to a lesser degree – consumer trends.

By understanding and keeping track of the various issues, news and events that impact gold prices, investors can build familiarity with the unique characteristics of the gold market, and over time, become better at sussing out upcoming price trends.

Intrinsic value and gold

Traditionally, fundamental analysis aims to discern the intrinsic value of a company’s stock. If the intrinsic value is higher than the current share price, the stock is considered undervalued, supporting the case to take a long position, with the expectation that the rest of the market will catch on that the stock is undervalued, and buy up the price to its “fair value”.

If the intrinsic value is lower than the current share price, the stock is considered overvalued. This could support the case for shorting the stock (or simply ignoring it), with the expectation that the share price will soon be corrected to bring the stock closer in line to its intrinsic value.

Understand that the intrinsic value of a stock is derived from the company’s business performance, financial health, perception of its leadership team, and regulatory environment – otherwise known as fundamentals.

However, gold does not have intrinsic value, as it does not have any of the characteristics of a company or business. It does not offer dividends, a right to future earnings or a promise of repayment at a later date. While the precious metal is acknowledged as an important commodity, supply and demand factors from manufacturing or commercial use alone does not reflect its intrinsic value. [2]

Rather, the intrinsic value of gold stems is ultimately arbitrary – gold is valuable because we say it is valuable. Its lustrous appearance, relatively rarity, difficulty of extraction and limited supply are all supporting factors that continue to make gold valuable in our eyes.

So if gold has no intrinsic value, then how do we apply fundamental analysis to the shiny metal? The answer lies in understanding gold’s history and role in our financial system.

For a time, gold was used to back currencies, acting as the backbone of the then-fledgling modern financial system. Although gold’s limited supply later made it too inflexible for the growing global economy, it has held on to its status as a precious commodity and credible store-of-value.

Thus, fundamental analysis of gold involves more geopolitical and macroeconomic factors, compared to fundamental analysis for stocks, which is generally more focused on the company itself.

5.2 Economic indicators affecting gold prices

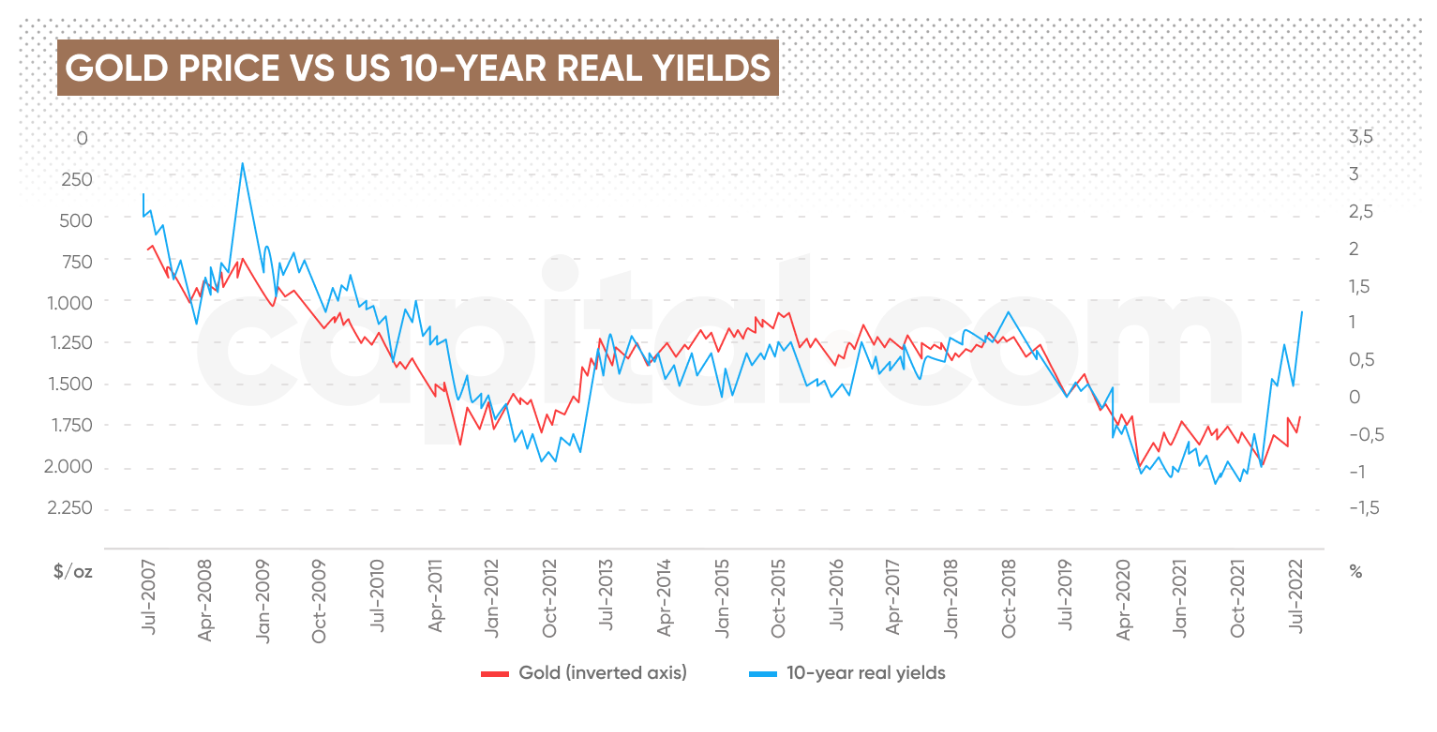

Inflation rate and central bank interest rate [3]

Inflation and interest rates are closely intertwined together – when an economy’s interest rate becomes too high, its central bank raises interest rates to slow down the economy and ultimately bring inflation back down to manageable levels.

During periods of high inflation, one popular move is to flock towards gold, due to its reputation as an inflation hedge. This is backed up by historical data which shows gold charting an annualised yield of 10.9% on average against nine major currencies, including USD, EUR and JPY. [4]

So yes, gold has the ability to hedge against inflation, and high inflation brings about high interest rates. That means high interest rates also means demand for gold must be high, correct?

Well, not so. In fact, gold should not do well in a high interest rate environment, and here’s why.

As an asset, gold does not offer a yield. US Treasury bonds do. Bonds pay out regular coupon payments based on US Federal Reserve interest rates. As such, during high inflation, bonds pay out higher yields, which is more attractive than the zero yields paid out by gold.

Hence, logically speaking, gold should not be popular in a high interest rate environment, as the incentive is to pile into bonds instead. This is indeed borne out by the data, which shows that when US Treasury Bond yields increase, the value of gold tends to decrease.

But this is true only to a point. When investors are not confident that central banks can rein in inflation, they turn once again towards gold in a bid to hedge against losing real value from safe assets such as bonds. This can happen when the inflation rate forecast outstrips the nominal interest rate, leaving holders of Treasury Bonds worse off.

In contrast, gold has a long track record as a store of value. The commodity enjoys a consistent level of demand around the world, enabling it to remain unaffected by market downturns in one or two regions.

Even should recession be widespread or global, gold continues to be seen as a valuable asset due to its liquidity and relative ease of cashing out during turbulent markets.

Read more about the relation between gold and interest rates.

Strength of the US Dollar [5]

Gold is denominated in the US Dollar, causing the two to share a unique relationship. Generally, the price of gold is inversely related to the value of the US Dollar. This is because all else being equal, a stronger US Dollar means gold is more expensive, which tends to suppress demand for the commodity.

On the other hand, when the US Dollar weakens, this means that gold becomes cheaper, as you need less US Dollars to buy the same amount of gold. Hence, this tends to increase demand for gold, pushing its price higher.

Incidentally, this observation that “when the Dollar weakens, the price of gold rises” is also why gold tends to be seen as a hedge against inflation. Inflation means prices of goods and services go up, which has the same effect as a weakening Dollar. Thus, as prices go up due to inflation, so does the price of gold.

Global economic stability [6]

During economic downturns, attention shifts to gold as investors seek to preserve their wealth from capital losses. This increased demand for the metal drives up the price of gold, strengthening its reputation as a safe-haven asset, which brings increased demand from more investors.

This can be seen during the stock market collapse of 2007, which saw gold achieve annual returns of 31.59% (2007), 3.41% (2008) and 27.63% (2009).

More recently, during the COVID-19 recession, gold achieved annual returns of 24.17% in 2020, followed by two negative years (-3.75% in 2021, and -0.43% in 2022). However, in 2023, amidst global uncertainty and slower-than-expected recovery, gold once again hit its stride, returning 13.08% that year. All returns are measured against the USD.

Geopolitical events [7]

The link between geopolitical events and the price of gold can be difficult to discern, as there is a fair amount of complexity involved. However, an analysis of historical data can help us draw some conclusions.

Firstly, it is true that geopolitical risks such as war, terrorism, and other destabilising events do tend to drive up the price of gold. However, in many instances, this rally does not last, and prices fall back to normal levels shortly after.

An example of this phenomenon can be observed during the 9/11 attack on the US, as seen in the following chart:

As you can see, while gold prices spiked in the immediate aftermath of the attack, prices went back to normal by mid-October. Here’s why: gold prices rise in anticipation of conflict, and when rumours turn into action, prices decline as investors take profit. In other words, a classic case of “buying the rumour, selling the news”.

Secondly, geopolitical events impact the price of gold to different extents, depending on where they took place. In general, events that did not affect the U.S. have a lesser chance of impacting gold prices.

See the following chart:

Two important dates to note here: terrorist attacks in Paris in November 2015 and in Brussels in March 2016. As you can see, these events had little to no impact on the price of gold. In fact, the commodity’s price declined in the wake of both incidents.

Historically, gold prices have acted in a way that reflects levels of market confidence. When the US carried out Operation Desert Storm in Kuwait, the net outcome of the campaign was to lower geopolitical risk in the Middle East. Thus, after an initial spike, gold prices fell back down as investors realised the campaign’s stabilising effect.

What these examples tell us is that while geopolitical risks can spark off gold rallies, they rarely last, and instead are likely to trend back down as the crisis passes or comes under control. Hence, it may not be wise for investors to pile into gold at the first signs of geopolitical trouble.

5.3 Market demand and supply

Prices of gold can also be driven by market demand and supply levels. Two of the biggest drivers in the gold market are jewellery companies and industrial applications, and of late, central banks. Let’s explore each one in turn.

Jewellery companies and industrial applications [8]

Worldwide, jewellery companies are the biggest driver of gold demand. In 2023, the jewellery fabrication sector accounted for 2,192.3 tonnes of gold, representing 40% of total global demand.

Hence, it should be expected that an increase in demand for gold jewellery would drive up the price of gold, due to the rarity of the precious metal and the difficulty in production. The two countries with the largest demand for gold by far are India and China. In contrast, in Asia and the Middle East, there is high demand for high-purity, investment-grade gold. [9]

Another main driver of gold demand is the industrial sector, in which gold is used for its high conductivity, non-reactivity and other unique properties. Electronics applications account for over 80% of gold demand in the sector, with the remaining distributed throughout chipmakers, nanomaterials research, space exploration and wearable diagnostics electronics.

In 2023, industrial applications accounted for 940.7 tonnes of gold, which is 21% of the global total. As such, advancements or breakthroughs in mass market electronics such as consumer products or healthcare devices can also drive demand for gold, which can cause gold prices to increase.

Central banks [10]

Gold makes up an integral portion of central bank reserves, offering diversification and a hedge against inflation. As there is no credit or counterparty risk involved with gold, the precious metal also serves as a source of trust in all economic conditions, making it one of the most crucial reserve assets across the world.

Central banks are a significant source of demand for gold, and collectively hold around 35,000 tonnes of gold, or about one-fifth of all gold ever mined since the beginning.

As such, when central banks increase gold buying rates, the heightened demand can drive up the price of gold. This can be seen most recently in 2022 and 2023, during which record-high demand from central banks were seen.

In 2022, central banks bought 1,089.1 tonnes of gold – a new record – and 1,037.1 tonnes in 2023, accounting for 23% of total annual gold demand in both years. During this time, the price of gold rose from US$1,800.1 per ounce to US$1,940.5 per ounce.

Gold mining and production

In 2023, gold miners supplied 3,363,2 tonnes of gold to the market, while recycled gold supplied a further 1,238.9 tonnes. This means that gold mining is still the major source of gold supply around the world.

Therefore, it stands to reason that disruptions in gold mining and production can have powerful effects on the price of gold.

For instance, delays in production due to war or geopolitical tensions are likely to cause price spikes due to lower supply. Central banks may also buy up more gold in anticipation of economic fallouts from unfavourable developments, further straining gold supply and putting upward pressure on price.

To keep up with developments in gold production, investors should follow news and reports from gold mining companies, including financial statements, which contain important data related to gold mining. Pay attention to changes in production levels and watch out for anomalies that may signal incoming price changes.

5.4 Financial reports and gold markets

Another source of financial reports on gold market trends and developments is institutional gold investors.

Large-cap gold ETFs and gold investment funds regularly release reports containing data, trends and analyses on the state of the gold market, making for a rich repository of valuable information for gold investors. These materials can help paint a picture of broader gold trends, providing an in-depth understanding of market characteristics.

Another type of gold-related financial report investors should seek out is the financial statements of gold mining companies and production firms. Such documents are not only important for sussing out gold production trends which can impact prices, they are also crucial in helping investors understand the performance and potential of publicly listed gold companies, many of which are included in popular gold ETFs.

5.5 Other events that may impact gold prices [11]

GDP growth, employment rates and consumer confidence

As we’ve discussed throughout this module, the price of gold tends to react inversely to economic results. We’ve seen how gold prices tend to spike in response to unfavourable readings such as high inflation, weakening US Dollar, and geopolitical crises.

Other economic indicators such as GDP growth, employment rates and consumer confidence may also affect the price of gold. If such readings are favourable, and consumers are comfortable spending, the price of gold tends to come down. This is because investors are drawn towards other risk-on assets such as equities and stocks, which tend to boom when the economy does well.

Monetary policy and interest rate announcements

Another factor to consider is monetary policy and interest rate announcements. When interest rates are low, demand for gold tends to rise as investors regard them as a more attractive alternative to government bonds.

Bonds and other fixed-income instruments offer lower returns in a low-interest rate environment, increasing gold’s competitiveness as a risk-free alternative asset.

Hence, when interest rates are reduced, gold demand increases, which may push up prices. In contrast, when interest rates are raised, bonds increase their yields, rendering gold – which does not provide a yield – less attractive in comparison.

Let’s not forget the impact of inflation rates. As mentioned earlier, when interest rates spike high enough to outstrip the nominal yield of bonds, gold tends to come back into favour for its ability to hedge against inflation.

5.6 Case study – A look back at gold in the past 10 years

From 2014 to 2024, there were two major economic crises that took place – the 2015 to 2016 Stock Market Selloff, and the 2020 Coronavirus Crash. Let’s take a look at how gold reacted to these events, concluding with a look at gold today.

2015 to 2016 Stock Market Selloff [12]

Also known as the Great Fall of China, the 2015 to 2016 stock market selloff was a global market downturn that occurred between June 2015 and June 2016. Although this event first originated in the Chinese stock market, a series of interlinked events saw global stock markets plagued by large selloffs as investor confidence dwindled.

Some of the contributing factors included:

- 2015-16 Chinese stock market turbulence, which saw a 43% drop in the Shanghai Stock Exchange Composite Index in two months, leading to the devaluation of the Yuan

- Shares selloffs around the world due to slowing GDP growth in China

- Petroleum prices hitting a six-year price low in August 2015

- The Greek debt default in June 2015

- The effects from ending of quantitative easing in the United States in October 2014

- A sharp rise in bond yields in early 2016

- And the Brexit vote that took place in June 2016

The Brexit vote was the final straw, and had the most dramatic consequences. Worldwide stock markets lost more than USD 2 trillion on 24 June 2016, making it the worst single day loss in history. Market losses continued to mount until a total of 3 trillion US dollars by June 27, 2016. [13]

How did gold perform during the 2015 to 2016 Stock Market Selloff?

This is a chart showing the performance of the S&P 500 (in black) vs gold spot price (in blue) for the period January 2015 to June 2017.

Between January 16 to November 16, gold clearly outperformed the S&P 500. 7 July 2016 saw one of the largest divergences between the two asset classes, with gold up by 15.87% compared to the S&P 500’s 1.47%.

This instance clearly demonstrates the impact of consumer sentiment on the price of gold. With stock market selloffs taking place across the world, and the worst single-day market loss in history, it can be surmised that consumer sentiment was at an all time low, with panic and fear ruling the markets.

True to its status as a safe-haven asset, gold shone brightly in the eyes of investors who started moving their wealth into the precious metal to weather the storm, explaining its stellar performance during the crisis.

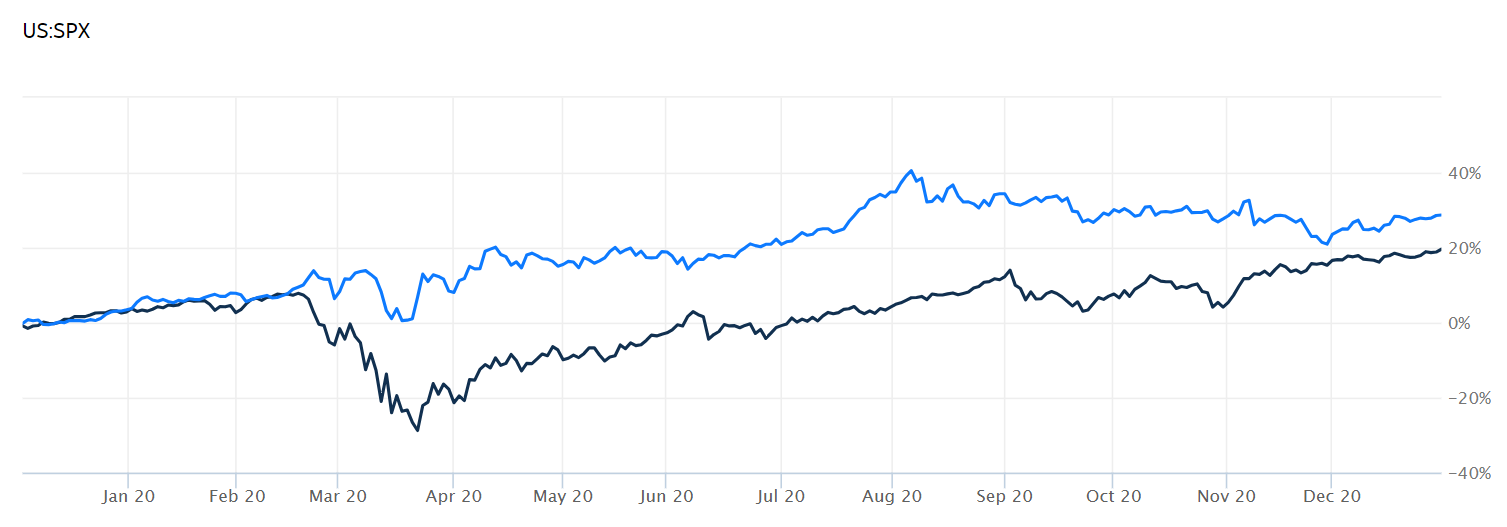

2020 Coronavirus Crash [15]

The 2020 Coronavirus Crash took place between February and March 2020, triggered by fear and uncertainty of the economic consequences of border closures, countrywide shutdowns, supply disruptions and the then-lack of a vaccine.

Although the crash itself was relatively short-lived, it produced three of the worst declines in US history. The Dow fell 7.79% on March 9; then fell by 9.99% on March 12; and finally, fell by 12.9% (nearly 3,000 points) on March 16, prompting several stock exchange suspensions that day.

It wasn’t until 24 November 2020 that US markets finally returned to January levels with the Dow passing 30,000 for the first time in history.

Finally, on March 16 the Dow plummeted nearly 3,000 points to close at 20,188, losing 12.9%. The drop in stock prices was so massive that the New York Stock Exchange suspended trading several times during those days.

How did gold perform during the 2020 Coronavirus Crash?

In this chart, we see the performance of S&P 500 compared to the spot price of gold. This is for the period between December 2019 and January 2021. Once again, the black line represents the equities market, and the blue line, gold.

We can see very clearly a sharp divergence from the moment the stock market crash happened, with the S&P suffering a steep decline. While the price of gold also went through a small dip, it was not as dire as equities.

During its lowest point on 23 March 2020, the S&P 500 read -28.77%; meanwhile gold was pulling upwards, reading +6.79%.

From that point onwards, gold continued to outperform the S&P 500, as the latter continued to trade sideways for the remainder of the year. It wasn’t until market confidence was restored and the S&P 500 went on a bull rally before the two asset classes closed the gap.

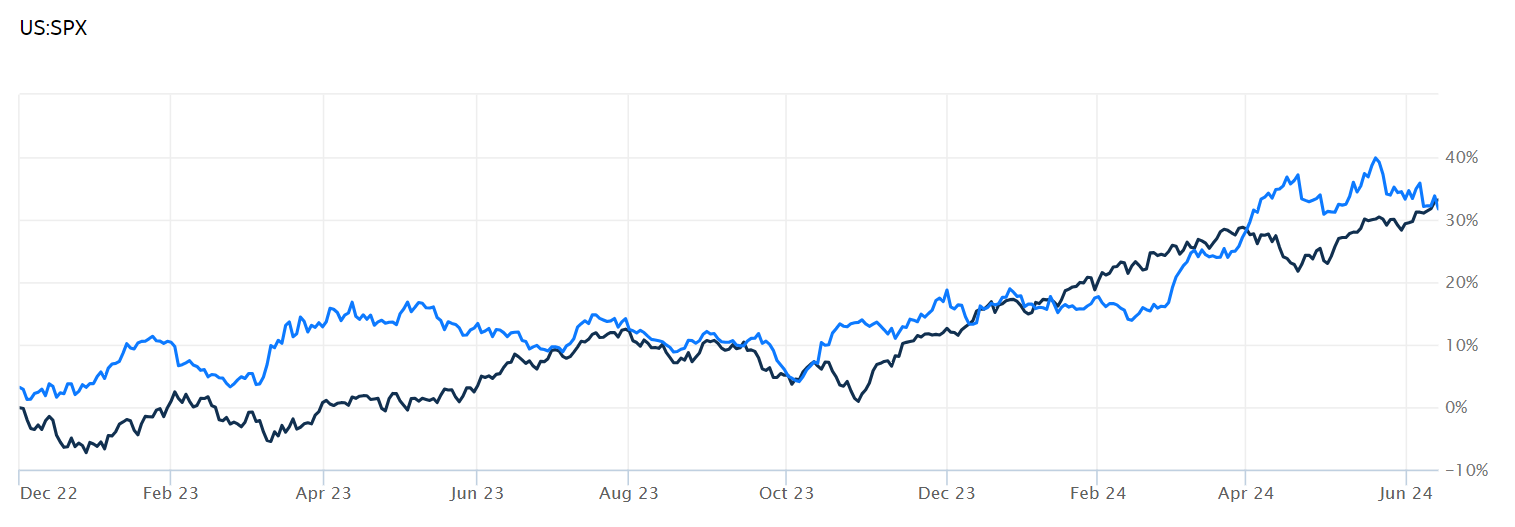

Gold vs S&P 500 after the Coronavirus Crash

Finally, let’s take a quick look at gold vs the S&P 500 after the market recovered from the pandemic recession.

This chart shows the performance of the S&P 500 (black line) vs gold spot price (blue line) from December 2022 to June 2024.

What’s interesting to note is that while the stock markets have well and truly recovered, charting record highs, gold seems to be doing the same. This runs counter to the theory that the price of gold is supposed to decline when the economy is doing well.

Yes, the economy is chugging along quite nicely, but there are still relatively high levels of fear and uncertainty. This is due to several factors, including:

- Inflation not declining as quickly as expected

- Prolonged war between Ukraine and Russia

- Hostilities in the Gaza Strip

- Houthis rebels attacking the Red Sea shipping route

- Waning hopes of US Federal rate cuts

- Increased buying of gold by central banks

- Sluggish recovery in China

- Slower-than-expected global recovery

All told, it seems that investors are adopting a cautious approach, preferring to stick with gold for its safe-haven status and high liquidity. With prolonged and increasing demand, it is no surprise that gold remains a top performer during these uncertain times.

Module recap

- Fundamental analysis is a core skill that all serious traders should learn. It is a method for determining the fair value of gold, understanding its price action, and can help with formulating trade ideas.

- When applied to gold, fundamental analysis involves studying and understanding various geopolitical and macroeconomic factors.

- Economic indicators can impact gold prices. Some of them include:

- Inflation rate and central bank interest rate

- Strength of the US Dollar

- Global economic stability

- Geopolitical events

- Being an important commodity, market demand and supply also impacts the price of gold. Three of the largest drivers of market demand are gold jewellers, central banks, and industrial applications. Meanwhile, the largest driver of gold supply levels are gold miners and production companies.

- Investors should include the following sources of information and data when performing fundamental analysis for gold:

- Financial statements from gold miners and producers

- Prospectuses and reports from gold ETFs and gold fund managers

- Economic reports such as GDP growth, employment rate and consumer sentiment surveys

- News reports on monetary policies and interest rate announcements

References:

- “Fundamental Analysis: Principles, Types, And How To Use It – Investopedia”. https://www.investopedia.com/terms/f/fundamentalanalysis.asp.

- “Gold Has No Intrinsic Value – Morningstar”. https://www.morningstar.co.uk/uk/news/120804/gold-has-no-intrinsic-value.aspx.

- “Investing In Gold: Is Gold Still A Good Inflation Hedge In A Recession? – Bloomberg”. https://sponsored.bloomberg.com/article/investing-in-gold-is-gold-still-a-good-inflation-hedge-in-a-recession-.

- “Annual Performance Of Gold And Silver – IGWT Report”. https://ingoldwetrust.report/chart-performance-table-gold-silver/?lang=en.

- “What Drives The Price Of Gold? – Investopedia”. https://www.investopedia.com/financial-edge/0311/what-drives-the-price-of-gold.aspx.

- “Historical Performance Of The Gold Spot Price Index – Curvo”. https://curvo.eu/backtest/en/market-index/gold-bullion?currency=usd.

- “Geopolitical Risk and Gold – GoldPriceForecast”. https://www.goldpriceforecast.com/explanations/geopolitical-risk-and-gold/.

- “Historical Demand And Supply – World Gold Council”. https://www.gold.org/goldhub/data/gold-demand-by-country.

- “Gold Demand Sectors – World Gold Council”. https://www.gold.org/about-gold/gold-demand/by-sector.

- “Why Central Banks Buy Gold – Reuters”. https://www.reuters.com/plus/why-central-banks-buy-gold.

- “How Do Gold Prices Affect the Economy? – The Motley Fool”. https://www.fool.com/knowledge-center/how-do-gold-prices-affect-the-economy.aspx.

- “2015–16 Stock Market Selloff – Scholarly Community Encyclopedia”. https://encyclopedia.pub/entry/36965.

- “Brexit-related Losses Widen To $3 trillion In Relentless 2-day Sell-off – CNBC”. https://www.cnbc.com/2016/06/27/brexit-related-losses-widen-in-relentless-sell-off.html.

- “S&P 500 – WSJ Markets”. https://www.wsj.com/market-data/quotes/index/SPX/advanced-chart.

- “The Coronavirus Crash Of 2020, And The Investing Lesson It Taught Us – Forbes”. https://www.forbes.com/sites/lizfrazierpeck/2021/02/11/the-coronavirus-crash-of-2020-and-the-investing-lesson-it-taught-us/.

Previous Lesson

Next Lesson